Condominium associations occupy a critical role in maintaining the economic health of community living spaces, balancing the delicate intersection of collective responsibility and individual financial obligations. Ensuring financial stability within these communities hinges on the timely and effective management of assessment collections—a process crucial for sustaining essential services and upholding community standards. This blog post delves into the pivotal question: when should a condominium association initiate the collection process to ensure adherence to legal frameworks and fulfillment of fiduciary duties? By exploring the legal mandates and practical steps necessary for initiating collections, we aim to provide a comprehensive guide to help condominium boards navigate this challenging yet essential aspect of association management.

Understanding the Legal Framework and Fiduciary Duties

According to Michigan’s MCL 559.165, condominium associations bear a contractual duty to enforce compliance with governing documents such as the master deed, bylaws, and rules and regulations. Failure to uphold these duties could result in breach of fiduciary duty claims, as evidenced in Highfield Beach at Lake Michigan v. Sanderson (331 Mich. App. 636, 954 N.W.2d 231, 247, 2020). This fiduciary duty encompasses various aspects of association management, including financial matters like enforcing rules, collecting assessments, and making sound business decisions, as highlighted in MCL 450.2541

Initiation and Execution of the Collection Process

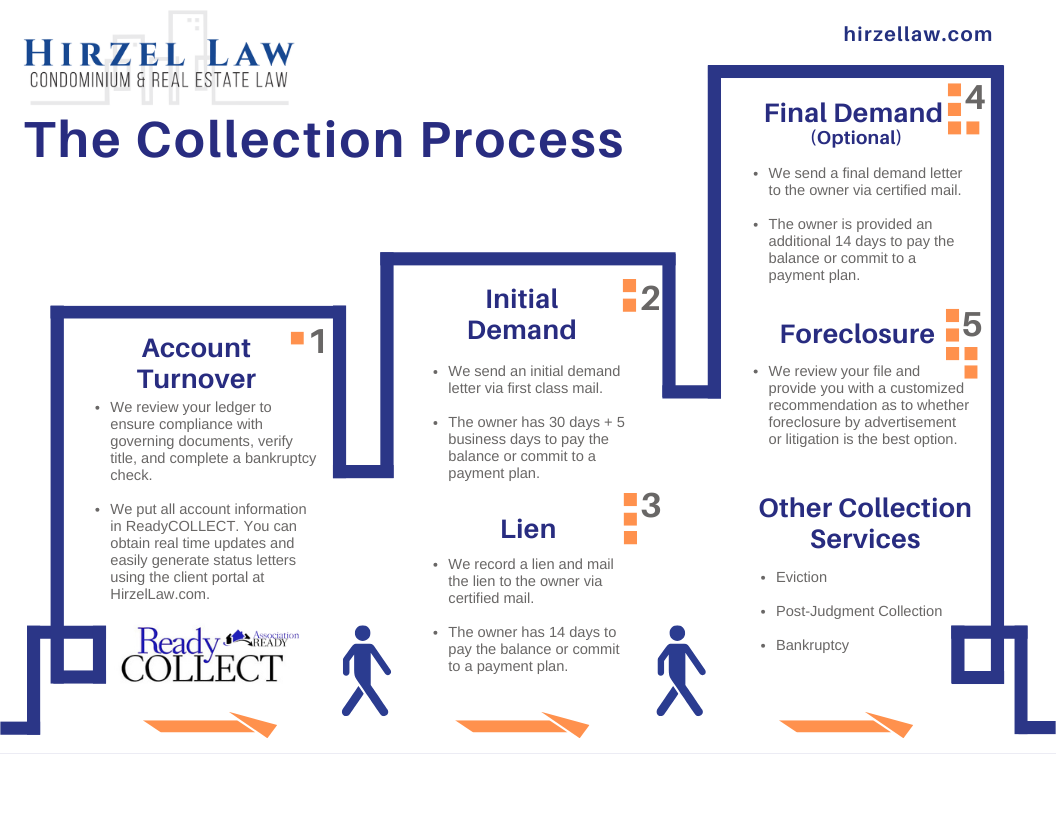

Typically, the collection process commences once assessments become delinquent, as specified in the governing documents. Whether assessments are due quarterly, monthly, or as a lump sum, the association should promptly send notices, usually within 30 days of delinquency. Waiting excessively—beyond 90 days—is discouraged to prevent exacerbating financial strain. Delaying until delinquency becomes a severe issue may hinder the association’s ability to obtain a proportionate remedy. In these notices, the association should clearly outline the delinquent debt, the amount due, and the deadline for payment. Additionally, it should define when assessments are considered delinquent, describe any fees charged by the association, and establish steps for collection, including required written notices. Furthermore, it should identify any third-party vendors, such as collections agencies and lawyers, involved in the collection process. For further insight, refer to “Unlocking Success: Using Legal Representation Over Collection Agencies for Delinquent Condominium Assessments.”

Upholding Fiduciary Duties and Implementing Robust Collection Practices

Condominium associations, bound by contractual obligations and statutes, must fulfill their fiduciary duty to collect assessments. This duty extends to safeguarding the association’s financial interests and ensuring equitable cost distribution among unit owners. Failure to enforce timely payments undermines economic stability and jeopardizes the ability to deliver essential services. For a comprehensive understanding of the collection process and its importance, refer to the Hirzel Law blog article titled “Delinquencies, Collections, and the Need for a Collection Policy.” Directors of condominium associations shoulder the responsibility of implementing and enforcing collection actions. They must act in good faith, exercise reasonable care, and always prioritize the best interests of the association and its members. This fiduciary duty encompasses various aspects of association management, including financial matters like enforcing rules, collecting assessments, and making sound business decisions. Establishing clear collection policies, promptly initiating the process, and ensuring adherence to contractual obligations are paramount for the financial well-being of condominium associations. By upholding their fiduciary duties and implementing robust collection practices, associations can safeguard their economic health and maintain a thriving community for all residents.

Conclusion

Hirzel Law expertly supports condominium associations in maintaining their financial stability through a meticulous and legally compliant collection process. This process involves initial reviews and checks, prompt and clear communication through demand letters, and decisive actions like liens or foreclosures if necessary. By ensuring that financial obligations are addressed promptly and equitably, Hirzel Law helps associations uphold their fiduciary duties, thereby fostering a financially healthy and thriving community environment. This approach not only safeguards the associations’ financial well-being but also protects the interests of all community members involved.